Consumer interest in plant-based foods continues to rise around the world. Personal health has gained importance over the past decade with the pandemic crisis accelerating a shift to diets considered better for physical and mental health.

A 2021 GlobalData online poll called Consumer Survey Insights: Plant-Based Preferences[i], explored market drivers in the industry. It found global consumers are more likely to limit their meat intake than exclude it altogether, with 27% following a vegetarian or a low-meat diet.

It also found Generations X, Y (Millennials) and Z are most engaged with low/no-meat diets, while Asian consumers are most receptive to plant-based alternatives, potentially driven by the traditional use of soy.

This new focus on health combined with growing awareness over the climate impact of the industrialised meat industry has prompted more people to reduce their meat consumption. Media campaigns, such as Paul and Stella McCartney’s “Meat Free Mondays’ have also helped to change behaviours.

Hype fades but plant-based not a fad

In response, leading brands have been innovating with plant-based ranges, using soy, grain and vegetable-based protein enticing consumers to explore meat substitutes.

Analysis from market intelligence firm GlobalData shows that the meat substitutes market grew at a compound annual growth rate of 11.7% CAGR between 2018 and 22[ii], driven by innovation, consumer interest and manufacturing demand but then hit some roadblocks in 2023.

Last year, a surge in production costs and steep retail price inflation clashed with a gush of plant-based meat-alternative product launches. The market stuttered and retailers shrunk shelf space for meat-free ranges.

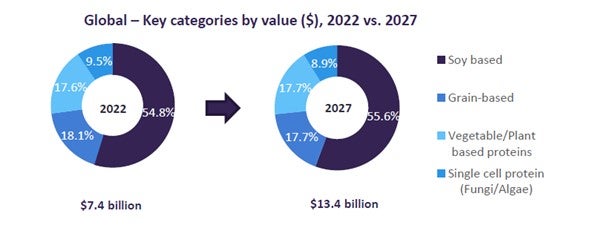

Yet despite these challenges, GlobalData foodservice analyst Ramsey Baghdadi says the meat substitute model is in rude health with growth to 2027 expected to be even faster than over the past few years. GlobalData analysis projects the value of meat substitutes to reach $13.4 billion in 2027, up from $7.4 billion in 2022.[iii]

A GlobalData report published last April identified the US as the biggest growth market for meat substitutes, with the market expected to reach $4.3 billion in 2026, more than double its value recorded in 2022. Outside the US, the report reveals Canada, Australia, New Zealand, Austria, Switzerland, Poland and Nigeria as some of the countries with the highest potential for brands in this category over the next few years.

In terms of categories, soy-based was the largest category in terms of revenue, accounting for a share of 55% of the market in 2022. Grain-based products ranked second, representing 18% of sales value. In 2027, GlobalData projects that globally, this split will remain virtually the same, but says appetite is decreasing for soy and grain-based products in most markets outside the US as concerns over how these ingredients are processed grow.

So, how can brands take advantage of this growing but highly competitive market amid rising sustainability concerns, supply chain challenges, emerging health risks of certain additives and commercialisation of cell-cultured meat?

Meal kits, personalisation and plant-based in foodservice

The rise of direct-to-consumer meal kits, which provide a range of meals – including soy-free, dairy-free, plant-based and gluten-free options – has been significant, driven by the convenience and range of products available online.

Ever more specialised and differentiated products are being introduced to cater to food allergies and intolerances, and consumers are willing to pay a premium for ‘better-for-you’ products, providing an opportunity for plant-based companies to launch more premium-quality ranges.

Plant-based products are thriving in the foodservice industry, with big quick service restaurant (QSR) names placing plant-based meat alternatives on their menus. Generation Z consumers are particularly responsive to these offerings. But the road ahead will not be straightforward for the market as the Russia-Ukraine war continues to create volatility in raw material prices and conflict in the Red Sea has the potential for hurting economic growth this year.

In addition, catering for growing demand for products made from sustainably farmed crops like algae and mushrooms and adopting green packaging will be expensive for the sector, already under pressure to price substitutes on a par with animal meat to increase mass-market acceptance.

GEA Food Solutions, a leading supplier of processing and packaging solutions for food, is working to support its customers to meet the growing demand for meat alternatives efficiently and in a sustainable way.

A strategic partner to the food industry, GEA develops with its customers new meat-free products and creates integrated process solutions.

For further information on GEA Food Solutions, download the whitepaper below.

[i] GlobalData: Consumer Survey Insights: Plant-Based Preferences, April 2021:

https://foodservice.globaldata.com/Analysis/details/consumer-survey-insights-plant-based-preferences

[ii] GlobalData: Analyst Briefing, May 2023 [iii] GlobalData: Opportunities in the Global Meat Substitutes Sector, April 2023: