A succession of bleak news stories from companies operating in the plant-based meat category has knocked brand and market confidence this year.

Nestlé has scaled back its presence in the market. Monde Nissin, the owner of Quorn Foods, has reported a slump in profits.

Smaller specialists on both sides of the Atlantic continue to go out of business.

And, in August, poster child Beyond Meat reported a 31% fall in second-quarter revenue, with its CEO claiming the category overall was suffering.

The negative headlines have resulted in some media outlets asking whether the meat substitutes market has seen its ‘bubble burst’.

Research and intelligence company GlobalData – Just Food’s parent company – questions those assertions. The company believes that, despite the current turbulence, the meat substitutes market has a positive future, albeit with much-reduced growth expectations.

The meat substitutes market is forecast to grow

Meat products remain by far and away more popular and, typically, more affordable than meat substitutes. However, globally 46% of consumers eat plant-based food between two to six times per week, according to a consumer survey conducted by GlobalData in the first quarter of this year.

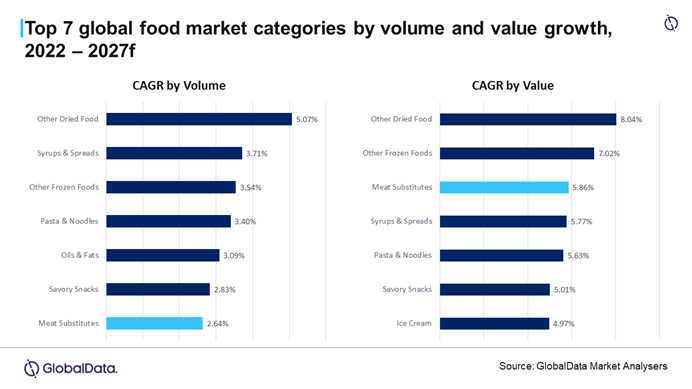

Driven by this cohort, GlobalData forecasts the meat substitutes market will achieve a volume CAGR of 2.64% and value CAGR of 5.86% over the period 2022 to 2027. Although the exceptional rates of growth once forecast for the category have eased, meat substitutes are forecast to achieve the seventh- and third-fastest food category CAGR in volume and value terms respectively through to 2027.

Within the foodservice channel, GlobalData’s growth expectations are even higher, with meat substitute volume sales forecast to grow at a CAGR of 3.85%. Based on operators’ buying prices, sales value is forecast to grow at 7.88%.

“This is an economically driven bump in the road for a relatively nascent category yet to live through its first real economic downturn,” Aaron Bryson, senior food analyst at GlobalData Consumer Custom Solutions, says. “In reality, what we are now seeing is category growth forecasts for meat substitutes falling in line with the normal growth expectations you’d see from other popular food categories.

“Indeed, given the current economic conditions, our forecasts for the meat substitutes market could decline still further. However, we believe that market forecasts will remain positive for meat substitutes albeit at low single-digit growth numbers until global economic pressures ease.”

A GlobalData consumer survey in the second quarter found 55% of consumers are either ‘extremely’ or ‘quite’ concerned about their financial situation. As a result, demand for more premium categories such as meat substitutes is weakening.

While macroeconomic pressures remain high, the category is likely to be subject to a rocky period until the global economy improves. However, brands and manufacturers can look to re-create the buzz that was once around their products by addressing key consumer questions about product recipes, health and wellness and the environment.

Health and wellbeing key driver for meat substitutes category

Despite the current economic headwinds, manufacturers and brands can take a more proactive approach to their consumer marketing and communications.

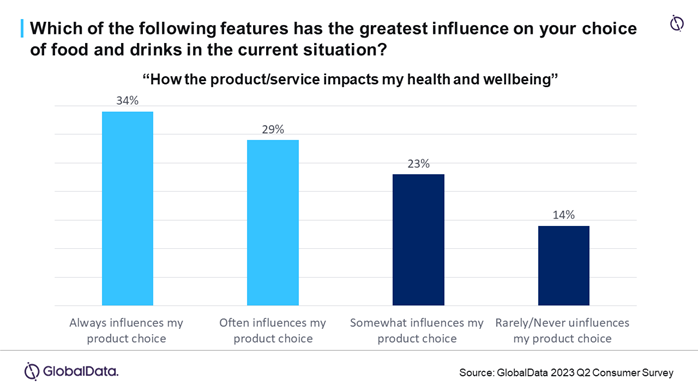

Health and wellness remains a core consumer concern when making purchase decisions. Asked in GlobalData’s Q2 2023 consumer survey ‘how the product/service impacts my health and wellbeing’, 63% of consumers said it ‘always’ or ‘often’ has the largest influence on choice. As such, meat substitute brands need to lean into health comparisons with meat, particularly in areas relating to calorie and fat content, but also health concerns about high meat consumption and conditions such as cardiovascular disease, colorectal cancer and type 2 diabetes.

Environment also important selling point

Environmentalism and animal welfare are core pillars in the development of the meat substitutes category. Brands and manufacturers can be much more vocal when communicating the ethical positioning of their products.

GlobalData custom research found 33.1% of global consumers state ‘animal welfare’ as a reason for consuming plant-based alternatives. It is claimed the intensive farming methods used to serve global meat demand create significant environmental, social and political issues, such as long-term damage to local water systems and soil, poor animal welfare and the removal of indigenous populations from their historic homelands.

Targeting younger cohorts

GlobaData’s Q2 2023 consumer survey found 10% of respondents between the ages of 16 and 34 stated they follow either a vegan or vegetarian diet, five percentage points higher compared to those aged 35 and over, highlighting the clear division in adoption between age groups.

Younger consumer groups are the key segment for meat substitute brands to target, especially as they will be more receptive to environmental messaging. This emphasises the importance of plant-based meat substitute brands effectively using social media to build relationships and brand awareness and educate consumers.

“Whilst opinions on meat substitutes remain polarising at this time the reality is, that further growth of meat substitutes is bound to happen,” Bryson adds. “Global food insecurity, and environmental and ethical pressures – stemming from intensive farming – are coming to a crescendo. The question is less if, but more when and by how much will the category grow over the next five to ten years.”

GlobalData combines in-depth technology and sector-level expertise in 20 of the world’s largest industries. Our consultants use this expertise to answer your bespoke questions with a custom solution that is tailored to your budget, timeline, and specific scenario. At GlobalData Consumer Custom Solutions, our consultants and analysts will work closely with you to understand your requirements and develop a tailored proposal and deliverables. Email us at consulting@globaldata.com or get in touch here.